Stock Market Forecast 2026

AI-powered stock market predictions for 30+ major US equities. Daily forecasts with 5-day price targets, expected returns, and confidence scores.

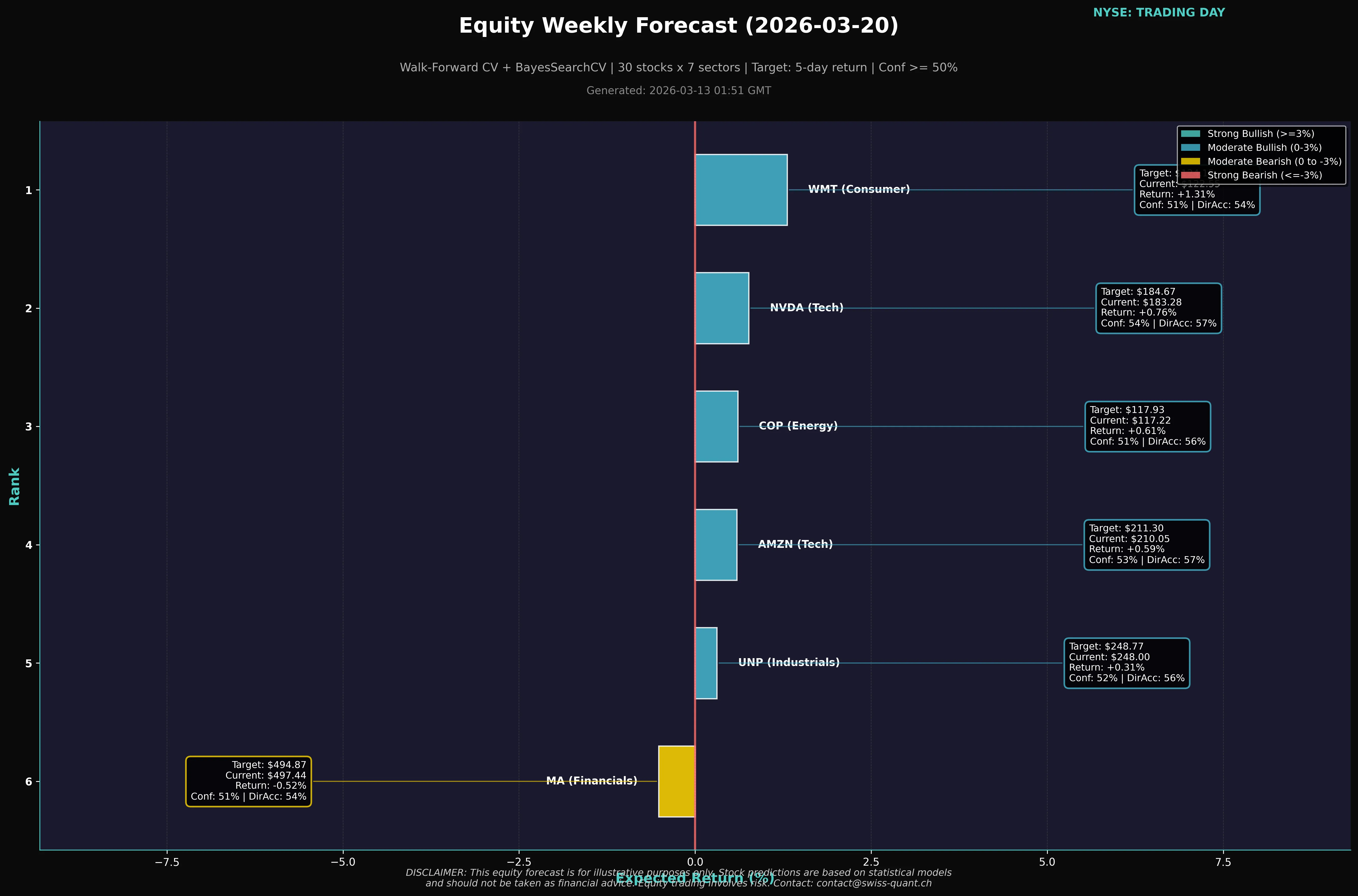

View Live Stock Forecasts →

Stocks We Forecast

How Our Stock Prediction AI Works

Swiss-Quant’s equity forecast engine uses an ensemble of XGBoost, LightGBM, and gradient boosting models optimized with BayesSearchCV hyperparameter tuning. The system processes:

Price Action Features

Intraday OHLCV data at multiple timeframes (15min, 1h, 4h, daily), volume profile analysis, support/resistance levels derived from pivot points, and price momentum across 5, 10, and 21-day windows.

Fundamental Signals

Earnings calendar proximity, SEC insider trading filings (Form 4), analyst consensus revisions, and sector rotation signals from ETF fund flows. These factors capture fundamental catalysts that pure technical analysis misses.

Macro Context

Federal Reserve rate expectations, VIX volatility regime, US Treasury yield curve, DXY dollar index, and ISM manufacturing data. Macro regime shifts significantly impact stock-level predictions.

Stock Forecast Accuracy & Transparency

Every stock prediction includes a confidence score, expected return percentage, and historical directional accuracy. Our models are validated using walk-forward testing on 200+ out-of-sample periods with purged cross-validation to prevent look-ahead bias.

We publish our full trading performance track record with verified results, so you can assess our model’s effectiveness before using our forecasts in your analysis.

How does walk-forward validation work?

Walk-forward validation trains the model on a rolling window (e.g., 180 days) and tests on the next 5 days, then slides the window forward. This mimics real-world trading conditions where you only have historical data. We also purge a 2-day gap between train and test sets to prevent data leakage from autocorrelated features.